Western Union

An old cigarette butt with one final puff to it

Key Data

Ticker Symbol: WU 0.00%↑

Price: $11

Market Cap: $4 Billion

Forward Dividend: $0.94

Dividend Yield: 9.1%

Payout Ratio: 40%

Areas of operation: Worldwide

Sector: Financial Services - Credit Services

Business

Western Union, WU 0.00%↑ , is an American multinational financial services company. Founded in 1851 the company dominated the American Telegraphy industry from the 1860s to the 1980s. In more recent decades they have transformed themselves into a wire money transfer service with a global footprint, facilitating the transmission of remittances internationally.

The company has 3 segments:

Consumer-To-Consumer

Business Solutions

Other

Of these, the Consumer-To-Consumer segment comprises the vast majority of revenues and operating income, with almost 90% of its revenues coming from it.

The Consumer-To-Consumer segment is primarily composed of cross-border money transfer services conducted through the company's retail agent locations worldwide, as well as its digital conduits.

As per the company:

Our revenues are primarily derived from consideration paid by customers to transfer money. These revenues vary by transaction based upon factors such as channel, send and receive locations, the principal amount sent, whether the money transfer involves different send and receive currencies, and the difference between the exchange rate we set to the customer and a rate available in the wholesale foreign exchange market, as applicable.

This is a fairly simple business model.

People have cash somewhere, and they want to give it to someone in a far away place. They go to a Western Union location, handover the money and tell Western Union “Please deliver this money to this person in this other country”, paying a small fee for the service.

This business is as old as international trade, and is a cornerstone of many countries' economies and communities.

The unit economics of the business is favorable with significant opportunities to get agents on the ground at low cost, since the capital expenditures to add a new agent are minimal, and the business can simply attach itself to an existing business rather than having to spin up its own Western Union store.

Indeed these favorable economics are mutually beneficial towards the businesses that partner with Western Union, since they can effectively add a new service and charge a fee for it, without it negatively impacting their ordinary operations.

That being said, the company is without a doubt on a down trend, and the reasons are mainly regulatory and due to increased competition.

On a regulatory basis there has been an ongoing and worldwide effort to restrict, surveil and control money and value transfers, not just internally within the banking system, but also across borders.

These efforts have manifested themselves in a number of different ways, from licensing requirements to impossible to fulfill Anti-Money-Laundering, to anti-fraud requirements, to simple bans and seizures.

All of these restrictions make transferring money less attractive, and add significant regulatory compliance costs to operating money transfer services.

Additionally throughout the years, and often in response to these restrictions, new competitors have come along that either entirely ignore these restrictions, or that are “piggy backing” off of these regulatory changes to build competing businesses to Western Union.

The company is undoubtedly in a decline, but the company is not remaining stagnant, and has an Evolve 2025 strategy intended to face these troubles:

In many ways this strategy is directly intended to take advantage of the company’s advantages, its Brand value and existing network, and use those to expand and improve on its up until now lackluster digital footprint.

The core idea here is to turn the existing Western Union customers from “one-off” customers, to an ongoing omnichannel relationship, by increasing the company’s product offerings to be more in line with its new competitors.

Will this work?

The company is expecting GAAP revenues to drop 10% in 2023, and from 2024 to 2025 to begin growing again by around 2%, while maintaining operating profit margins around 20% like today.

These aren’t good numbers, and it’s difficult to call this a turnaround story, when it’s fairly clear that 2025 earnings will be lower than 2022.

Personally I don’t even really buy the 2% revenue growth in 2024 and 2025, I think there’s every chance that the company will continue to shrink going forward.

But does this mean that the company is worthless? No!

The unit economics are favorable, and even with a shrinking business, so long as the company is profitable and cheap enough it may well make sense to buy!

I’d call this a classic “Cigarette Butt” play in the style of Ben Graham, where the business is going down, but there’s still one last puff to it if you buy at the right price.

Management

Devin McGranahan is President, Chief Executive Officer, and Director of The Western Union Company, having joined the company as its CEO in late 2021. With more than 25 years of experience in business, he joined Western Union from Fiserv, Inc. where he was the Senior Group President of Global Business Solutions.

With a lot of experience in the financial sector, and with some very successful digital platforms under his belt, Mr. McGranahan has the background needed to bring this centuries old company into the digital age.

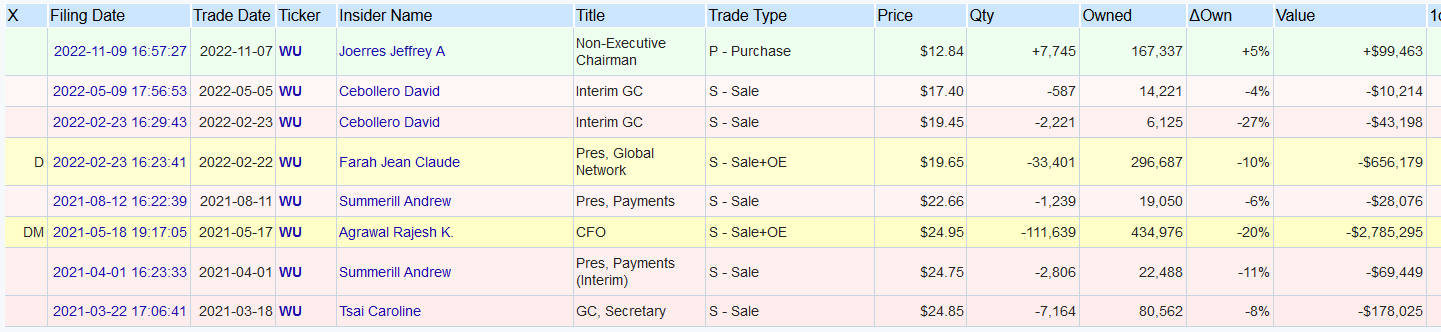

From an insider sales perspective the company has seen little movement over the past few years, and although there have been plenty of sales these have happened at much higher prices.

More recently we see an insider increase his position in the company at prices quite a bit higher than they are trading now.

I wouldn’t put much stock into these trades.

Key Risks and Opportunities

Risks:

High regulatory risks

Evolve 2025 will likely not be successful

Highly competitive industry

Opportunities:

Asset light

Favorable Unit economics

Reliable and centuries old business is unlikely to be fully disrupted

Financial Data:

Shareholder Returns:

Dividends

The company pays a $0.97 dividend.

The company means to maintain its dividend.

The payout ratio is around 50%

Share Buybacks

The company conducts regular share buybacks

The company has bought back $360 million in shares in 2022

Shares outstanding have reduced by 5.2% in 2022

Income Statement:

Revenue Growth Rate

Long Term - (2.8)%

3 Year - (8)%

Revenues are likely to continue shrinking.

Pre-Tax Profit Margins

Long Term - 18%

Return on Assets

Last Year - 10%

EPS Growth Rate

Long Term - 4%

3 Year - 23%

Cyclicality

Non-Cyclical

Cash Flow Statement:

Operational Cash Flow Growth Rate

Long Term - (8)%

3 Year - (34)%

Investing Cash Flows Growth Rate

The company has booked substantial proceeds from selling its B-2-B segment

There are no major capex

Financing Cash Flows Growth Rate

Substantially all operating cash flow is being returned to shareholders via dividends and buybacks

Balance Sheet:

Assets:

Main Assets are cash and funds held for clients.

About 30% of the company’s assets are goodwill and other intangibles.

Liabilities:

The main liabilities are the client funds mentioned above.

There are $2.6 billion in borrowings

Debt:

The weighted average effective interest rate on all borrowings is around 3.9%

No Debt Cliffs in the next 2 years.

Valuation:

Key Metrics:

Bullish

Discounted Earnings - $15.8

Discounted Cash Flow - $14.22

Margin to PE - $52.11

Market Multiple - $44.33

Cash Multiple - $44.63

NCAV - $0.92

Bearish

Discounted Earnings - $5.29

Discounted Cash Flow - $4.76

Margin to PE - $26.17

Market Multiple - $9.81

Cash Multiple - $13

NCAV - $0

Average

Discounted Earnings - $9.65

Discounted Cash Flow - $8.69

Margin to PE - $33.72

Market Multiple - $28.67

Cash Multiple - $28.70

NCAV - 0

Expected Value:

First, a few things to note about these valuations:

I’m assuming revenues will drop by 9% forever.

I took away 400 million in revenues and 50 million in earnings from the B-2-B segment

This is a very bearish assumption and I don’t think it’s all that realistic, and it shows primarily in the discounted earnings and discounted cash valuations.

Changing the expected revenue growth rate to 0% would essentially double both of those valuations, and I feel like this is a fairly reasonable stance to take (and even more bearish than the company's guidance).

Regardless though I think a declining business might justify an additional margin of safety in terms of its revenue assumptions, and -9% revenue every year is a fairly conservative assumption.

When we aggregate all this, we get a fair value of around $18, with a safe purchase value of $12.77.

The company is currently trading at around $11 which I find to be significantly undervalued.

Investment Thesis

The company has an old and proven business model

Regulations and new competitors are causing trouble in the business

The new management may well turn it around

The business is consistently profitable

Revenues will decrease significantly

The company is very cheap, and this is a “Cigarette Butt” play

Decision

Current Stance: BUY

I don’t currently own WU 0.00%↑ , but I will open a position this month. Ultimately the company is in no danger of bankruptcy, and it has demonstrated a commitment to returning capital to shareholders.

EDIT: I have since opened a small position at $10.68 per share.

While it’s true that it is a declining business, the unbelievably low price combined with the consistent profits and capital returns to shareholders make owning this business an attractive proposition for at least a few years.

If the company goes to around $40 it may become overvalued, and be worth selling. But unless that happens, I will be happy to cash in the dividends and just hold it.

Do you have a different view on the company? Are you buying, selling or holding?

Let me know what you think down below!

Thank you Tiago for sharing your analysis. I really enjoy reading your weekly updates!

This is an interesting pick and I'm now curious to research WU more. Curious to hear what's your take on the 2 billions of Goodwill on the Balance Sheet? That's half the current market cap, and 25% of their assets. WU seems to have made several acquisitions over the years, and it's hard in retrospect to find out how these played out.