The Search for a Durable Competitive Advantage

Profit Margins and why they matter

Companies exist to make money for their owners.

That’s a controversial statement in some circles, socialists for example tend to think companies should exist for the benefit of society as a whole. Syndicalists think they should exist for the good of their workers. Tech company founders and Venture Capitalists rant and rave about how their companies are about making the world a better place.

Many of these people have good intentions behind it. After all, I don’t think a lot of people are particularly happy about human misery, and these people see companies as a way to help alleviate that.

The problem with that is that when a company has a second role as the doctor, teacher and caretaker for its workers or its clients or the society it is in, then it may have to stay in business long past its time to call it quits just so it can keep on fulfilling that role.

This, as counter intuitively as it may seem, is a bad thing, because it means unprofitable companies will continue plodding along, taking up resources that could be better used elsewhere.

If a steel manufacturer can’t make steel cheaply enough to pay for its operations, then it is being out-competed by its competitors and will soon either turn around or shut down.

But if that same steel manufacturer is forced to remain in business, it will be a drag on the society that will have to pay for its inefficiency in higher prices, for its workers who could be doing something better, and most importantly for its owners who could and should be investing in the next great company, rather than being tied to this anchor.

An unprofitable company is not a good thing for anyone, least of all its owners.

If you look at the total return of the stock market over the past 100 years what you will find is that profitability, that is, earnings, have composed just about 100% of the long term return.

This makes sense, after all companies have value because they provide their owners with a return on their investment, and that return will ultimately need to come from the earnings the company makes in its day to day operations.

So how can we identify these profitable companies?

We look. Everyday you interact with dozens of companies many of which are publicly traded, from the shoes you wear to the food you eat, someone has made it and gotten paid for it.

Have a look around your house, see which brands you like most and check if they’re a public company. If so, you now have a good reason to research that company and if everything comes up good, invest in it!

The important thing is for you to make an informed investing decision, at the end of the day, it doesn’t matter if you really like the sandwhiches from that store down the street if the store that sells them is losing money.

Fortunately nowadays it’s actually quite simple and easy to get clear and accurate data directly from the source. Most publicly traded companies have an Investor Relations section to their websites where you can freely download all the data that those companies are required to make public.

For those that don’t have a website, or whose filings are hard to find in their website, the Securities and Exchange Commission has a website where you can download them.

Companies in the US (and in most other jurisdictions) are generally required to file a number of reports detailing their activities, these reports often include some key financial statements, and the one we will be analyzing today is called “The Income Statement”.

To be more specific, we’re going to be talking about and analyzing the profit margins of a handful of businesses, and seeing what that tells us about that business, their competitors and most importantly whether or not we should invest in them!

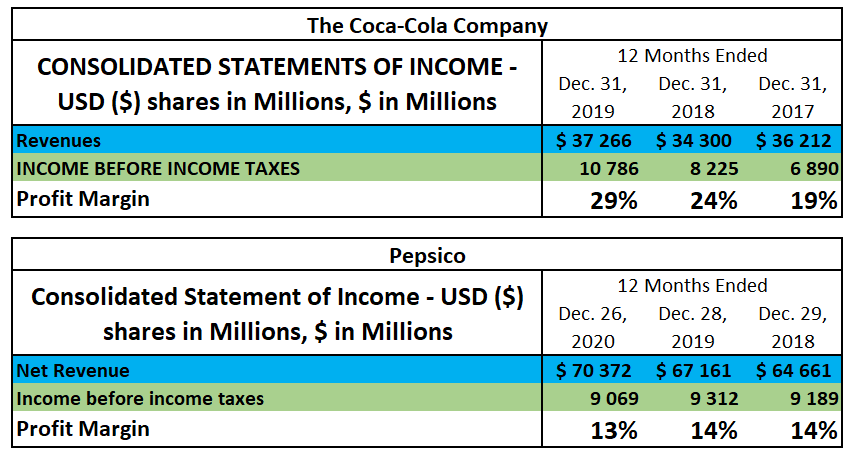

Let’s take 2 examples of longstanding blue-chip companies, The Coca-Cola Company ($KO) and Pepsico ($PEP). Let’s see their Income statements side by side:

At first glance this might seem complicated, but if you stick with me you’ll see its actually fairly simple to understand. I’ve highlighted all of the important parts we will be discussing in this post.

The first thing you’ll notice is how the income statement differs between $KO and $PEP.

You’ll find some items under Coca-Cola that doesn’t show up under Pepsico, for example Pepsico has a “Pensions and other benefits” item just below “Operating Profit”, whereas Coca-Cola doesn’t.

The reason for this is due to slight differences, both in expenses and incomes, as well as different impacts on the bottom line of some items.

The Basics

If you look at the Light Blue item, titled “Revenues” or “Net Revenue”, you will find the first important number you will want to keep in mind. This corresponds roughly to the total amount of cash that the company has taken in during the period.

Generally speaking investors want this number to increase year after year, though even the best companies sometimes have a down year (or two!), so its usually best to look at long term trends. Here we see that Coca-Cola had a decrease in 2018, but they made that back in 2019.

In Orange you will find the Gross Profit, that’s essentially your Revenue minus the costs of the goods you sold. For Coca-Cola that’s the money they make from selling syrup minus the cost of making that syrup.

In Grey you can find the Operating Income. You can think of it like the profit that the company makes in its day to day operations, without including expenses like interest payments, taxes, and other expenses that aren’t directly related to their business.

In Green you find the Income before Income Taxes, this is the profit upon which the government is owed taxes. This is the key metric to watch because with very few exceptions all investments has to pay taxes, and so its useful to consider them in equal terms.

Finally in Yellow you have the Net Income per Share, this is the after-tax earnings that you as a shareholder are entitled to for owning a single share.

What to look for

It’s very nice to know what these numbers mean, but how do we use them to compare investments?

Clearly in our two examples above, $PEP had greater revenues than $KO, does that mean its a better company to own?

But then if you look at the Income Before Income Taxes, we can see that it was about the same total amount.

And the income per share is completely different, despite their income before taxes being similar.

Well, the reason for that is because the companies are different. They have different amounts of shares, they have different revenue streams,for example $PEP sells more than just Pepsi, they also sell snacks and other types of consumer goods. All of this affects their costs, and the revenue they make.

Not to mention the amount of money they make is different, as are their expenses.

In order to be able to compare them we will need to figure out what question to ask, and then do some simple math to get the answer.

Profit Margins

You can think of profit margins as the answer to a simple question:

Out of every dollar my company earns, how many cents are mine?

The way I calculate it is very simple, you simply take the Income Before Income Taxes and divide that by the Total Revenue.

So lets calculate them for $KO and $PEP:

As you can see, $KO is generally significantly more profitable than $PEP, with their profit margins hovering around 25%, whereas $PEP usually holds steady around 14%.

The reason this happens becomes apparent if we look at the rest of their income statement.

If we calculate the Gross Margin, or in other words, how much the products they sell cost to make, we can see the following:

We can see that for every dollar earned by $KO, around 39 cents is spent buying the ingredients to make the syrup they are selling. On the $PEP side, that’s around 45 cents.

Here again $KO has an edge, but not as big of an edge as the Profit Margin would lead you to believe at first.

The difference between Gross Margins is only around 6 cents, rather than the average 11 cents when it comes to their overall Profit Margin.

So where is the difference?

And here we see where the issue lies. $PEP has significantly higher Selling, general and administrative expenses than $KO. These are expenses related to wages, marketing, and really all other costs related to their business that aren’t the costs of the goods themselves, and $PEP has a lot more of them than $KO.

In fact, 40% of their revenue goes right out the door to pay these expenses!

So what does this mean?

Is $KO really better than $PEP? What makes a good Profit Margin? What should we look for in a company? Should we just buy the company with the biggest margins?

Well, first of all let us be clear, the higher the Profit Margin the more profitable the company can be.

Higher Profit Margins show that the company is either in a market without much competition, or that it has a significant amount of pricing power that it can use to generate profits.

Both of these are good things for a company and the investor that owns it, and an indication of the existence of a Durable Competitive Advantage within a business.

Generally speaking companies with Profit Margins above 20% have some form of Durable Competitive Advantage, whereas companies with profit margins below 10% are either troubled companies, or companies operating in a very competitive market where they don’t have a lot of pricing power.

In this particular case, if we’re going by the numbers I would say $KO is a better company, however that doesn’t mean $PEP isn’t also a good company, and it certainly doesn’t mean you’d be better off buying $KO over $PEP no matter the price.

The price is the key thing to look at here, after all, even if buying $KO gives you 11 cents more for every dollar than $PEP, if you can buy more dollars of $PEP than you can of $KO you would still be better off.

After all, if for the same price it costs you to buy 1 dollar of $KO earnings, you can buy 2 dollars of $PEP, well… Two times 15 cents equals 30 cents, which is 5 cents more than the 25 cents you’d get from $KO.

What i usually do to calculate which company is a better deal is the following:

This way you get a simple number that lets you compare companies. The higher the value, the more bang you’re getting for your buck.

After all, a company that has consistently high Profit Margins should have some sort of advantage that others don’t, which would make them a safer company to buy.

Intuitively too it makes sense that a company with higher Profit Margins would be more attractive than one with lower, even if it is slightly more expensive. After all, you’re paying more for a higher quality company.

Now this isn’t perfect, and I’m certainly open to feedback on how to change this way to value companies, but to me this sort of equation makes sense, and is one that i mean to use going forward.

Of course, even without comparing companies we should set some standards for what we’re willing to pay for.

Generally i set this limit at 66%, that is, the result of that formula should be 0.66 or higher for me to invest in the company. In order for me to go below that, I would need a good reason.

This means that at the current price and latest earnings, the results for $KO and $PEP are:

$KO - 0.89 at $48.97 and a PE of 28

$PEP - 0.55 at 129.19 and a PE of 25

The results

So, $KO is a better company by the numbers, right?

Well this is where it gets tricky because not everything is necessarily the result of the numbers in the Income statement. There is after all a whole bunch of other financial data in both the Balance Sheet and the Statement of Cash-flows that also has a role to play.

Furthermore even in this Income Statement there are still certain things that might seem like an issue, but might actually provide some tailwinds going forward.

$PEP for example has significantly higher General Expenses, this is what is really cutting into their margins, but if we go back a couple of years so did $KO.

In fact the thing that has allowed $KO to jump ahead in margins in the past few years has been the fact that they have been aggressively cost cutting those expenses.

Given the extra “fat” $PEP has there, they might be able to make significant advances in their margins if they begin to aggressively cut costs in the near future. This would give $PEP a boost that $KO has already gotten, so to speak.

Additionally, the difference in businesses that both companies are involved in also affect their margins.

Yes, $PEP snacks business is not as profitable as the sugary drinks business, but it provides some measure of protection when their Pepsi sales take a downturn, as we’ve seen over the last year...

Overall I’m not yet outright discarding one of the options. While $PEP doesn’t follow one of my rules, i feel there are legitimate reasons to still consider it as a reasonable investment going forward.

If you have any questions or comments, shoot them on Twitter @TiagoDias_VC or down below!

I’ll see you next week!

Why use 2017-2019 for Coke but 2018-2020 for Pep?