The Problems with Discounted Cashflow Models

Why I don't buy the bullshit

Many investors use Discounted Cash-flow Models as the cornerstone of their valuation, indeed many of them outright state that such models are the only method of valuing companies.

While I do think that discounted cash-flow models have some use, and that they can certainly provide valuable insight into the value of a business, I also think that they have some serious issues that make their use require a pinch of salt and skepticism in order to be accurate.

What’s a Discounted Cash-flow Model?

According to Investopedia, a Discounted Cashflow Model is:

Discounted cash flow (DCF) is a valuation method used to estimate the value of an investment based on its expected future cash flows. DCF analysis attempts to figure out the value of an investment today, based on projections of how much money it will generate in the future. This applies to the decisions of investors in companies or securities, such as acquiring a company or buying a stock, and for business owners and managers looking to make capital budgeting or operating expenditures decisions.

This might seem complicated with a lot of different jargon that someone who has no background in finance and mathematics will be left with no clue as to what it means.

That said, at it’s core a discounted cashflow is simply doing 2 things:

Find out how much cash a certain investment will generate over its lifetime

Find out how much that cash is worth

It’s really that simple!

Using our old One Man Corporation Example, if the investment is an Axe, we just need to see how many more trees we would be able to chop with the axe, and then figure out how much those extra logs are worth.

Learn how to make your own

Of course that’s a very simplified description of how it works, and it tells you nothing about how to make your own.

I’m also not a professor, and I don’t think I’d be able to accurately teach such a subject over my weekly blog…

If you’re not yet familiar with how these models work, you need to learn first, otherwise the next few sections won’t make much sense.

For that, you’d need to take some valuation classes at a university… Or alternatively skip the part where you’re paying thousands to attend a university, and simply watch Professor Damodarans classes on youtube!

This is literally undergraduate and MBA level schooling, given by a professor in a classroom setting, that you can use to learn for free! If you prefer newsletter style content, you’re in luck! He also writes a newsletter on substack!

We live in an age where anyone, anywhere on earth can have access to some of the best education for free, from the comfort of their own home, and at their own time and pace.

The Core Proposition of Cash-flow Models

The core way cash-flow models work is by assuming a growth rate for revenue growth, from which you remove the cost of acquiring that revenue.

That cost of acquiring that revenue includes capital expenses, as well as COGS, etc…

Then, you take that value, and discount that by a certain discount rate, usually that discount rate is taken from interest rates, a weighted average cost of capital, or some other method that helps you value how much less a given dollar will be worth in the future.

The exact specifics of how each of these numbers change from model to model, and ultimately it doesn’t really matter.

Why do I say this?

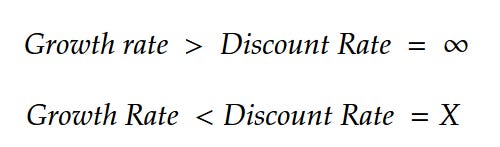

Because at its heart these models are simply a matter of the difference between the growth rate in cash-flows, compared with the Discount rate.

If the growth rate in cash-flows is higher than the discount rate, you will get an infinite value for the business.

If the growth rate in cash-flows is lower than the discount rate, then you will get a specific dollar value for the business.

That’s all a discounted cashflow model is doing.

So of course if you make small tiny changes in either of those 2 variables, you will get wildly different values for the business, even when the underlying business hasn’t changed a thing!

The problem

Tell me this, does the value of a shoe store change when the interest rate paid by the 10 year treasury bond changes?

Do they sell less shoes when such rates go up a fraction of a percent?

Do they have to pay more for the shoes?

Do their employees have their wages adjusted to the interest rate?

Would a corner-store shoe shop owner have his life and business affected by this change in interest rates? Would he even notice that such rates were 1% in the morning and 1.25% in the evening?

No?

Then why the hell do the valuation models somehow think that the business has lost all of its value?

This is the core problem with discounted cash-flow models, at their heart they forget that this is a business, not numbers on a spreadsheet!

These tiny changes in interest rates, or costs of capital are often small and transitory and yet they have a disproportionately high impact on the supposed value of the business.

On the other hand other less easily measurable, and more qualitative indicators of business quality are either left by the wayside, or wholly ignored because they are hard to measure and quantify.

How much more valuable is that shoe store because its worker spent 10 minutes talking with a kid about the shoes he was looking at?

If all you’re looking at is a Discounted cash-flow model, then not at all.

Now don’t get me wrong, I’m not saying quantitative methods are bad! I’m not saying we should be incorporating additional variables of “customer loyalty” and “employee satisfaction” into valuation models. Those are both terrible ideas.

What I’m saying is that there are so many assumptions, and so many extraneous variables where even small changes causes changes in either the growth rates or the discount rates, that the models are made useless.

Coming back to the 10 year treasury example from earlier, how useful is the spot price of that treasury?

It’s really not useful at all in valuing a business. Now a rolling 10 year average of that might be somewhat useful, but it too will pale in comparison to other factors.

Don’t use spot values as inputs to Discounted Cash-flow models.

This includes, but is not limited to the following:

Interest Rates

Costs of capital

Capital Structures

Inflation

Earnings and revenues

etc…

All of these things wildly change over time, even for the same company, and those changes cause wildly different values for a business.

If your discounted cash-flow model is spitting out wildly different values on a quarter to quarter basis, all you have is a shit model.

Don’t do this crap.

Don’t lose sight of what you’re actually valuing, a business with earnings and assets.

Keep it simple.

The simpler you go, the less assumptions you make, the more likely your model will be on the ballpark, and that’s really all you want.

For retail investors like me, and even for professional investment firms, you should have a sufficiently high margin of safety to make small changes in valuation meaningless.

By all means do your cash-flow model, but also do a dividend discount model, and an asset based model, and Ben Grahams models, and other models that actually make sense given the underlying business.

Do all those, and if they are all around the same ballpark, then chances are the business will likely be worth about that much.

Then take 30% from that value, and only buy if its below that.

You should not be adding complexity, particularly where that complexity is only adding additional points of failure.

In short, the problems with discounted cash flow models are:

Irrelevant variables - how often does that business lend cash to the US government for the treasury rate to matter?

Arbitrary Assumptions - Why are you setting your expected growth rates at 10% instead of 9.25%?

Spot values - What makes you think last years earnings weren’t an outlier?

Blindness to the Business - Why would the same models work for fundamentally different businesses?

Am I wrong?

Spot on! And what about getting info on customer satisfaction reviews to get a better idea how the company is doing?