The One Man Corporation - Part 1

How a corporation works

Imagine for a moment that you are a one man corporation.

The business is simple and understandable, you will be chopping down trees and selling the logs for cash.

The proceeds you will use to pay your expenses, and whatever is leftover will be reinvested into the business, or distributed to the shareholders as dividends.

Taking this simple example, let us see how running this business works, and what we should be looking for as an outside investor looking in.

Incorporating

The first thing you’ll need to do is to actually incorporate your corporation. You may be its only owner (and employee) but corporations are entities that are legally distinct from their owners.

For the sake of simplicity let’s say that there is no cost to incorporating (or maintaining) a company.

The first thing you’ll need is to have some equity in the company (in some places that’s called “Social Capital”). This is essentially what the company actually owns, or for a new company like this it’s what you’ve put in to the company.

There are plenty of rules on how to do this, and it differs from country to country, so i will not go into details.

For the same of argument let us say that your newly create company is started with $1000. That’s how much equity you have in the company, and what you’ve put in from your hard earned savings.

Let’s also say that the company is split into 100 shares, such that each share owns 1% of the company.

With $1000 in shareholders equity, divided by 100 shares, that means the book value for your newly created corporation is $10 a share.

For now you own all 100 shares, but this might change in the future.

Here’s what your One Man Corporations’ balance sheet looks like right now:

Starting the Business

So you now own a corporation, but all that corporation has is $1000 in the bank. Keeping money in the bank might be safe, but it doesn’t generate all that much revenue, so you need to use that money to actually get a business going.

You’re going to be chopping down trees and selling the logs for some cash, so let’s see what you need:

An Axe to chop trees with

Some Trees to chop down

An Employee to do the chopping and selling of the logs

This is a pretty simple business after all, and you don’t need much to start off.

If you wanted to start a plane manufacturing company you’d need a lot more stuff (and capital) just to get started on building your first plane!

Fortunately you’re just chopping down trees and selling the wood, so those 3 things should suffice for now.

Even better though, you already know who you’re going to hire to do the chopping and selling… Yourself!

Of course you need to eat and have a roof over your head, so let’s just say that you’re taking a salary of $1 for every tree you chop down, and a commission of $0.5 for each log you sell.

You also need some trees to chop down, luckily you know a guy with some forest that wants to get rid of the trees there.

So you agree to pay him $1000, in 2 tranches of $500 each for the right to chop down the trees in his land, and keep the logs. You pay the first tranche now, and the rest in 6 months.

Finally you will need an Axe to chop down the trees. You know you’re going to need a good one, so you splurge a little bit and spend 200$ on a decent one that will last you a few years.

Here’s what your balance sheet looks like right now:

Note how the assets equal the liabilities and the shareholders equity put together. That’s how you know you haven’t screwed up somewhere in your accounting.

In this case what you did was take $200 of our cash asset, and convert it into an “Axe” asset worth $200.

You did the same thing with our “Right to Chop Trees on Land” asset that is worth $1000, however in that case, since you only paid $500 and still have another payment due in 6 months, you have a “Outstanding Land Payment” liability.

This is effectively your $500 debt that we have to your friend who lets you chop and keep the trees.

Additionally, if you have a look at the “Cash and Equivalents” you’ll note that you now only have $300 in our corporations bank account. This is why you insisted on the 2 tranches of payments for the right to chop trees.

If you hadn’t done it that way, you wouldn’t have had the cash to pay your employees or to buy the Axe.

You’re hoping to use the cash that the company generates in the first few months to get the cash needed to pay the rest.

This is called cashflow, and it’s a pretty big deal, after all, even if your company is profitable and provides good services, if it doesn’t have cash at the end of the month to pay its bills, the company will be doomed.

Cashflow problems are the number one cause of bankruptcy, so always keep a keen eye on it. It never hurts to have some cash in the bank!

In this case, we need to make $300 in 6 months, otherwise we’re in trouble and will have to sell our assets to pay off our debts (or raise more cash).

The first month

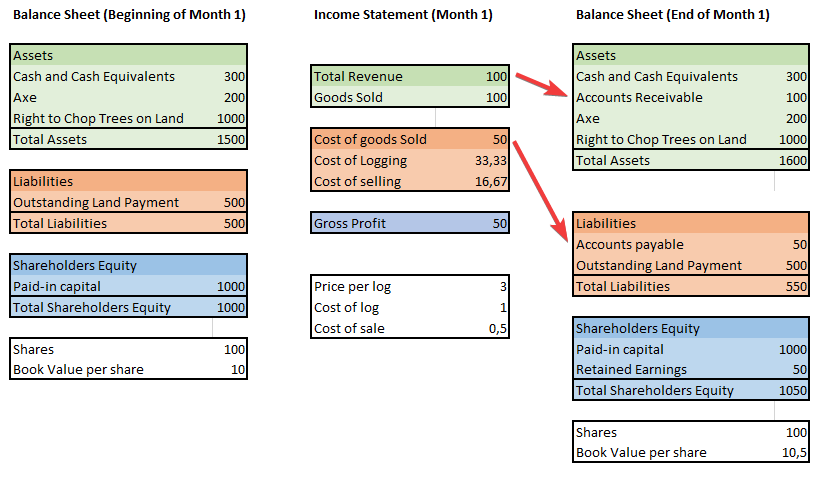

Let’s have a look at the numbers for your first month in business:

That’s a lot of numbers, isn’t it?

If you’re confused, don’t worry about it, it’s actually pretty simple to understand.

On the left we have the company balance sheet at the beginning of the month, and on the right we have its balance sheet for the end of the month.

If you’ll recall the balance sheet is simply a list of everything the company owns, and everything it owes at a given point in time. You can make a balance sheet for every day of the year if you want to, but companies generally stick to making one at the end of each quarter.

In our case we just want to see the progress of the company throughout the month, so we just make 2 with a 1 month difference between them.

In the middle, you have the income statement. It’s essentially just a list of everything you made and spent throughout the whole month.

In this case, the income statement tells you sold $100 worth of logs, and that cost you $50 to do it. That means you came out with a gross profit of $50!

Where did that profit go in the balance sheet showing the end of the month? Right where the arrows are pointing!

The revenue is shown in the “Accounts Receivable” section, because your client has already received the goods, and the funds are on their way. Once they arrive they will go to the “Cash and Cash Equivalents” section.

The expenses are in the “Accounts Payable” section, because you already owe your employee the money for the work he (you) did, but you haven’t transferred it over yet. When you do, you’ll be removing that cash from the “Cash and Cash Equivalents” section of the assets, and zeroing out the “Accounts Payable” section.

Since you now have $50 profit you didn’t have before, your shareholders equity has also gone up by $50 to $1050!

This makes your book value per share go from $10 to $10.5!

Looks like everything is on the up and up, and soon you’ll be living it up with the likes of Jeff Bezos and Bill Gates!

Or is it?

Have we accounted for everything here?

Could we have forgotten something?

Non-Cash Expenses

What we’re missing is Non-Cash Expenses.

These are Expenses that we have that don’t cost us cash, at least not in the short term that is being shown here.

This includes things like Amortization and Depreciation, which we have here.

Depreciation is the loss in value that your assets suffer over time and use. Amortization is similar to Depreciation.

In this case we need to depreciate our Axe as well as our right to chop trees.

The reason for this is simple, and is most easily seen with the right to chop trees. At the beginning of the month we had 12 months of tree chopping rights, but now we only have 11. This means we lost 1/12th of its value, or $83.33, because we’ve used up 1/12th of its lifespan.

The case for the axe is similar, even though the Axe doesn’t have a set expiration date like the Right to Chop Trees, that axe will lose value over time. It will chip and become less effective over time, and eventually it will break.

In this case, lets assume the Axe has an expected lifespan of around 5 years, and so we will depreciate accordingly to the tune of $3.33 a month.

The Depreciation of the Axe and the Tree rights will go into the “Accumulated Depreciation” line in the Liabilities section.

When we add that in we see that we didn’t actually make a profit, we actually made a loss! Sure we have more cash in the bank than we did at the beginning of the month, but our earnings are negative.

So you didn't actually made a profit, you made a $37 loss!

Depreciation is a real actual thing, if you don't account for it, then in 1 year your Tree Rights will expire, and you won’t be able to replace them. The same thing will happen with the Axe in 5 years.

Something needs to change in this company, and we will talk about that next time!

Let me know what you think, and comment down below, or tweet at me. I am always open to listening to other views.

I’ll see you next time!

Love it. Accounting in simple words. At the beginning of my entrepreneurial journey I too forgot about some of the above topics and almost went bankrupt