Pay Yourself First

Or why you should see investing as a monthly expense

We have been talking a lot about specific companies, analyzing them, seeing how much they are worth, and deciding whether to buy them or not.

We’ve also seen and talked about how a company works from the very basics, and while we haven’t discussed all that there is to discuss there, today i want to discuss something else.

Personal finance is the foundation of every investor, and understanding not just how to invest, but how you spend your money is a key pre-requisite to be financially free.

Let’s discuss your personal budget, your mindset as an investor, and the exact concrete actions you should take in order to build wealth.

The Mindset

“Pay yourself first” is an investor mentality and phrase popular in the personal finance and financial independence community.

Essentially it means that you should automatically route a specified amount of money from every paycheck you receive to some sort of savings or investment when you receive it.

This sort of automatic savings contribution happens before you begin paying your monthly living expenses or making discretionary purchases.

By automatically removing the money from your bank account, you force yourself keep your expenses under control, reducing discretionary impulse purchases, and ensures you have a steady stream of income that is 100% dedicated to investing.

I wholeheartedly support this idea, and I go even further in saying that the vast majority of your paycheck should be allocated to settle your expenses even before it hits your bank account.

To do this you should have a clear, concise and written budget for every month, that you keep an eye on regularly, and that you do not deviate beyond your defined parameters.

The Budget

Making a budget is one of the best things you can do for your financial health, and the best thing is that it doesn’t cost you anything other than a bit of time.

The first thing you need to do is to get an idea as to what your average income is, and what you spend it on.

For most people, or at least for me, my income is almost 100% from my salary.

The rest is job bonuses or tax returns, these are uncertain incomes and so i usually ignore it on my month by month income, and so should you.

Never plan your life on uncertain income. Let it be a pleasant surprise.

The next thing you need to do is figure out what your expenses will be. Some of these expenses are very predictable, you know (or should find out) what your rent is. Likewise, your utilities and similar services should be somewhat predictable.

For you other expenses, just have a look at the last year of bank statements, classify them into the different types, and you’ll get a decent idea of where your money is going.

You should separate these expenses into Discretionary and Non-Discretionary expenses.

Discretionary expenses are things you can do without, like going out to dinner, or the cinema.

Non-Discretionary are things you can’t do without, like your rent and your groceries.

Of course if you spend all of your money every month, you won’t have any left to save, invest and build wealth.

The easiest wait to make sure you don’t forget about it, is to make sure that every month you invest a set amount.

How much is that small amount? 15% of your take home pay is a good ballpark.

If that is too much for you, then you need to seriously re-evaluate your spending and income, in particular your big expenses like rent.

If your rent and utilities is above 30% of your take home pay… You need to seriously consider move somewhere cheaper.

I’m sorry if it sounds harsh, but ultimately your ability to build wealth and live a comfortable life will be impacted if you are paying too much for rent, dining out, or any other thing.

You must watch your expenses, and if you’re so hard up for cash that you cannot reliably set 15% of your income aside, then you need to get yourself out of that situation as soon as you can.

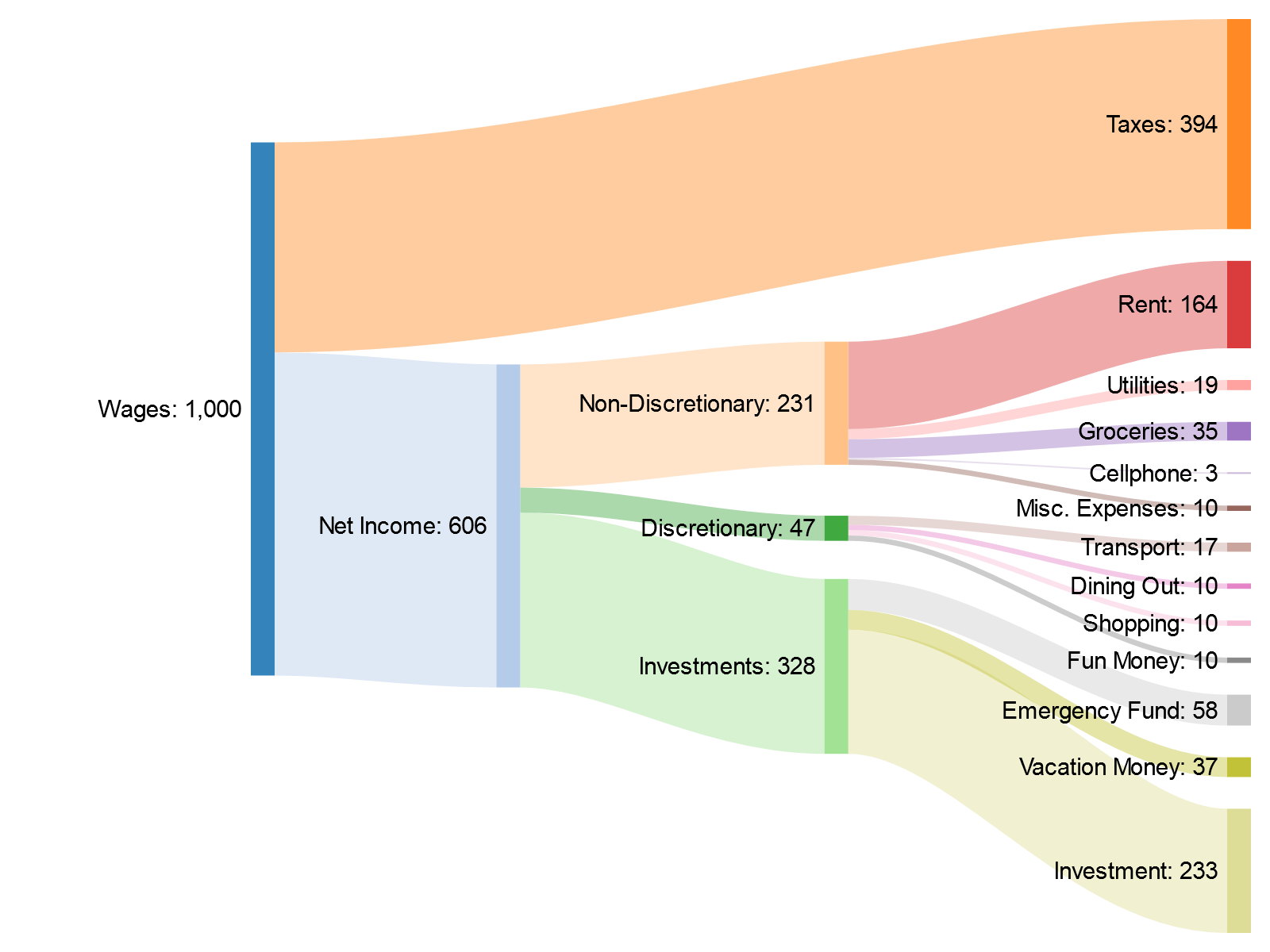

My Budget

Everyone’s budget is different, but I thought it might be a bit interesting to break down mine into its components, and talk a little bit about it.

Having it split in 100 percentage points is not granular enough, so here is its split on a “Per Thousand” basis:

So you can see that Taxes are the biggest slice, taking on almost 40% of my income.

Mind you this “Taxes” section is only including Income taxes, while I don’t have a clear view of just how much total taxes I end up paying, due to the multiple tax rates on different things, and the effects on the entire supply chain of everything I buy, I can make an estimated guess that out of my Pre-Tax Income roughly 50% is spent on taxes.

In other words, for every Euro that goes into my pocket, I put one more Euro in the states coffers.

The reason I account for these sorts of taxes is simple, it allows you compare expenses on a dollar for dollar basis.

Some countries have significantly different income tax rates, and most countries have some sort of progressive tax system.

Each of this will result in different amounts and percentages of ones income to be paid in tax, so its important for us to be aware of that amount.

Taxes kill most forms of wealth creation, so be aware of them, and settle your affairs in a way that will protect your ability to generate wealth.

If you have tax advantaged accounts, use them. If you have tax deductions and exemptions find them and check if you can’t save a few dollars there. This is probably the best possible thing you can do for your financial freedom.

As for the remaining expenses, I’m fairly frugal.

When it comes to Non-Discretionary Expenses, my rent is around 27% of my after-tax income, on the high end but still manageable and below the maximum 30% we discussed earlier.

I live in a high cost of living area, so this can’t be helped, but I am seriously considering purchasing a home, at least that way I would be using that portion of my income to build wealth, rather than simply throwing it away every month. Something to think about…

Of the remaining non-discretionary expenses I don’t have much. Groceries form the bulk of it, with utilities, cellphone, and other miscellaneous expenses coming in after.

In terms of discretionary expenses you’ll see i don’t have many.

Discretionary expenses are by their very nature those most easy to cut back on, since they are fundamentally optional.

Going to theaters, bars, restaurants, etc.. may be fun and enjoyable, but ultimately you need to ask yourself if it is worth the expense, and not just consider the money out of you wallet today, but the money that money could have become in 5, 10 or 20 years from now, having compounded itself over time.

To me, it’s generally not worth it, so my expenses there are low.

The Investments Section is the largest one, primarily because i make it a priority to take care of it.

The “Investment” section is the largest, and corresponds to my regular monthly deposits into my brokerage that i immediately use to Dollar Cost Average into my positions, which i split 50/50 between wide market index funds and individual holdings.

If you are not confident in selecting individual holdings, or just don’t want to spend the time and effort researching and keeping up to date with them, I would suggest just sticking with monthly purchases of low cost index funds.

The rest I split between “Emergency fund” and “Vacation Money”.

The vacation money is self explanatory, it’s cash i set aside every month so that once or twice a year I can take a relaxed vacation, travel a bit and have some fun.

This is money that I expect to spend throughout the year, but which might be available in case some emergency happens.

The “Emergency Fund” is how much i “Top up” my emergency fund by if it is not sufficiently funded.

To be more specific, I keep an emergency fund big enough to fully fund 7 months of Discretionary and Non-Discretionary expenses. If the emergency fund is already fully funded, I simply add it to my monthly investing activities.

Some of you might think this is too much, and that might be true, I don’t think there is any real risk of me going 7 months with zero income anytime in the near future, and in any case I live in a European country with fairly extensive social security and other programs.

That being said, I am fairly conservative, and don’t trust social security to do what is best for me.

My prior experiences with such systems have unfortunately validated my views there, and so I prefer to keep a larger than average emergency fund at hand, this way, if the worst happens I won’t be caught out waiting for a handout from the state that will never come.

What your next steps should be

Now that you’ve seen how I handle and view my finances, I would encourage you to take action today and make your own budget.

It doesn’t need to be perfect, but it does need to be done.

Get your bearings, find out what you make, what you’re spending it on, and use that information to your advantage.

Define how much of your income you will set aside to invest, and do it regularly and in the amounts you are confortable with.

It’s not difficult, all it takes is discipline and commitment.

Make your budget, stick to it.

Do you agree? Do you disagree?

Let me know what you think!

And as always, if you have any questions or comments, shoot them on Twitter @TiagoDias_VC or down below!

I’ll see you next time!