Olvi Oyj ( OLVAS HE)

A fairly valued alcohol company with potential upside

Key Data

Name: Olvi Oyj (OLVAS HE)

Sector: Alcohol

Share Price: 29.60 €

Dividend: 1.20 €

Market Cap: 612 Million €

Areas of Operation: Finland, Baltic Countries, Belarus

Business:

The parent company Olvi plc holds 100 percent of the Estonian brewery AS A. Le Coq, 99.88 percent of the Latvian brewery A/S Cesu Alus, 99.66 percent of the Lithuanian brewery Volfas Engelman, 100 percent of the Danish Bryggeriet Vestfyen and 96.36 percent of the Belarusian brewery Lidskoe Pivo. Olvi plc holds 100 percent of Servaali Oy which is a leading import, sales and marketing organization for premium beverages in Finland and 100 per cent of The Helsinki Distilling Company.

This is effectively a holding company for a Finnish brewery, alongside a number of other breweries based in the Baltic countries and Belarus.

This is a “multi-local” company that grows primarily through acquisitions and whose profits derive from adjusting their products to local tastes and by leveraging localized brands.

This is not a global business like Carlsberg or Diageo, it’s purely a regional competitor focused almost entirely on the eastern baltic region.

The company has 3 main regions:

Finland

36% of Sales

26% of profits

The Baltic Countries

47% of Sales

32% of profits

Belarus

21% of Sales

43% of profits

The company produces the following drinks:

Beer (53% of volume)

Soft Drinks (15% of volume)

Water (11% of volume)

Kvass (9% of volume))

Long Drinks (5% of volume)

Cider (2% of volume)

Juice (2% of volume)

Other (3% of volume)

The company owns a number of brands and breweries, and uses them to produce and market their products. Most of these brands are old, with longstanding community bonds, some of which have existed for hundreds of years.

As a whole, alcohol is a really stable and mature business, with regular cash flows and high returns on assets.

Historically this has been a relatively stable business with 10% profit margins pre-covid, however margins have meaningfully worsened since.

That said the management team is aware of it, and has made it a solid priority to get those back up, which combined with the doubling in revenues seen since 2019 will (if successful) result in double the earnings.

That doubling in revenues is actually quite an interesting thing. The company has averaged over 10% growth in revenues for the past 5 or so years, which is pretty amazing and attributed to a combination of additional volume and price increases, as well as a handful of acquisitions.

Finally, and importantly, the company has a clean balance sheet with effectively no debt, maintaining only operating liabilities. This provides an additional margin of safety that i like, while giving management the option to leverage up if they happen to find a good acquisition, or want to “juice up” the returns to equity.

This is actually something they highlighted in their latest quarterly report:

M&A expectations

We stated in strategy that we have preparedness to go forward with selected M&A activities in Europe that support strategy implementation. Olvi Group is net debt free so growth can be accelerated with debt too.

I’m fairly ok with this, since they have been mindful of their acquisitions so far, and if they can find a nice bolt-on acquisition to complement their existing brands I think the added risk is worth it for the additional growth.

Important Notes

Background

The underlying business is fundamentally solid, and I don’t expect any major disruptions there, but that doesn’t mean that the stock is rsik-free, or without issues.

Every company has its warts, and Olvi Oyj has two:

Multiple Share Classes with a controlling shareholder

The Belarusian Business

Lets begin with the simple one, the Belarusian business.

As mentioned above the company’s business in Belarus accounts for 21% of its revenues and 43% of its profits, but as I’m sure you’re aware relations between Finland and Belarus aren’t exactly in the up and up given the conflict in Ukraine.

The company has already suffered from fines (which may have been politically motivated), and due to sanctions doing business in Belarus has become significantly harder.

Nor is capital flows to and from Belarus currently possible (and may not become possible for the foreseeable future), and of course there is always the danger of full on expropriation.

As the company stated in its report::

The business operations and financial forecasting in Belarus continue to involve considerable uncertainty. For example, the uncertainty concerns the development of exchange rates, the unpredictability of the operating environment, local legislation and taxation, trade sanctions, and the functioning of financial transactions with Western countries. Olvi’s subsidiary operates independently in Belarus and finances its operations with cash flow from its own operations.

During 2024, legislative changes have been implemented in terms of dividend payments and laws preventing the sale of companies. The payment of dividends abroad by Western-owned companies has been restricted for 2024–2025 by setting regulations on maximum amounts. According to the current interpretation, the dividend that the Belarusian company can legally pay to the parent company is around EUR 1–3 million annually in 2024 and 2025. Despite legislative changes related to the prohibition to sell, the sales restrictions concerning shares in Olvi’s subsidiary remain in force. Olvi has no permission to sell shares in its Belarusian subsidiary. We are actively following the legislative situation.

The market has noticed this, hence why the share price tanked upon the beginning of the conflict.

Personally I think that this is probably priced in? I don’t think the market is valuing the Belarusian business at all when looking at comparable businesses, and so the way I see it, if international relations normalize, that would likely provide a decent catalyst to a higher valuation.

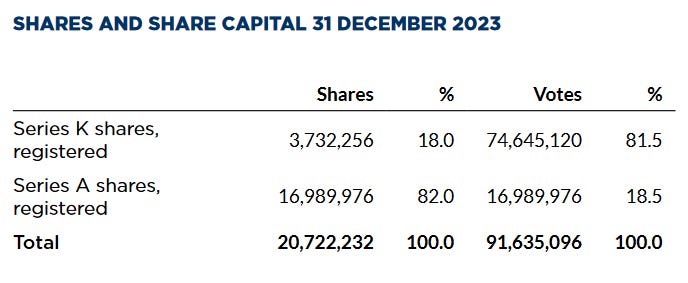

The bigger problem is really the elephant in the room. The dual share class structure.

There are 2 share classes, A and K shares. Both classes have the same economic rights, but K shares have 20 votes per share, compared to the 1 vote per share of A shares. Only the A shares are publicly traded.

As you can see, despite K shares having only 18% of economic rights, they hold 81.5% of voting rights, presenting a serious mismatch in incentives.

Worsening this is the fact that there is a controlling shareholder:

Olvi’s principal owner is the Olvi Foundation, which is a non-profit foundation. Olvi’s long-term managing director and principal owner E.W. Åberg and his wife, Mrs. Hedwig Åberg established the Foundation in 1955.

The Olvi Foundation gives out from Olvi’s dividend yield 2-3 million euros annually in grants, scholarships, awards and prizes. Among other things, the Foundation supports activities for the youth and the elderly, study opportunities and local community work. It also promotes the development of the utilisation of natural resources and food economy.

This effectively means you’re at the mercy of the whims of a non-profit foundation, which might interfere with the operations of the business, without suffering the full effects of that interference.

Ultimately this means getting control of the company is effectively impossible, and so we must value the business accordingly.

This is a classic case where a Dividend Discount model is appropriate to use, which is why i used that method.

Key Indicators:

Revenue Growth CAGR: 8%

Net Margin: 6%

Return on Assets: 7%

Return on Operating Capital: 8%

Return on Equity: 13%

Debt to Assets: 44%

Book Value per Share: 14.37 €

Cyclicality: Non-Cyclical

Expected State: Stable

Current Valuation:

Price to Earnings: 15.3

Price to Book: 2

Price to Tangible Book: 2

Price to Revenue: 0.9

Shade Research Valuation:

Assumptions:

Discount Rate: 8%

Starting Dividend: 1.20€

Dividend Growth Rate: 4.7%

Unlike most other valuations on this newsletter, this one was fairly simple and formulaic, I simply used the growing dividend discount model to get the output value.

The reason for this is simple, there is no way for me to ever acquire control of the business, and the reliable dividend makes the growing discounted dividend model the best option to value a stable and growing business like this.

I did fiddle with a few things though.

The discount rate that I arrived to was 8% and it is effectively a CAPM discount rate with a few changes:

Risk-Free Rate: 2.2%

Equity Risk Premium: 5%

Beta: 0.8 (historically this has been 0.45)

To this I added my standard 30% margin of safety, making the 8% discount rate used above.

The reason for the increased beta is to reflect the added risk regarding the Belarusian operations.

This resulted in a value of 37.42€ per share, well above the current market price.

Results

Ultimately the company is undervalued for the type of business that it is, with a potential trigger to a valuation bump if EU-Belarusian relations improve.

There are 2 main issues with the stock as an investment:

The discount rate, though appropriate for the business is relatively lower than what I usually use

The controlling shareholder rubs me the wrong way

I’m uncertain at the moment. I actually like the company, and the investment, but I’m not really sure if the return matches my required rate of return.

That said I don’t think investors will do poorly here.

My Current Stance: BUY