Microsoft Corporation - Part 2

Valuing this Software Company

Last week we had a look at Microsoft, an American Software company with a large and diversified business, which despite earning more in revenue than most countries GDP, has still grown both revenue and earnings at a massive 11.36% Compound Annual Growth Rate.

Today, we’re going to take a look at the company itself, and we’re going to value it to see if it’s at a reasonably affordable price.

, with the company name appearing to its right.")

Key Financial Data

The first thing we should take care to know before we do any sort of valuation of Microsoft is to review the past few decades of data and use that to determine a few different ratios and knowledge.

Here’s the bit and pieces that I feel are most important:

I’ve split this into 3 sections, Margins, Growth and Per Share metrics. There are a few other things that are also important and that we will be discussing later on, but for now let’s talk about these things.

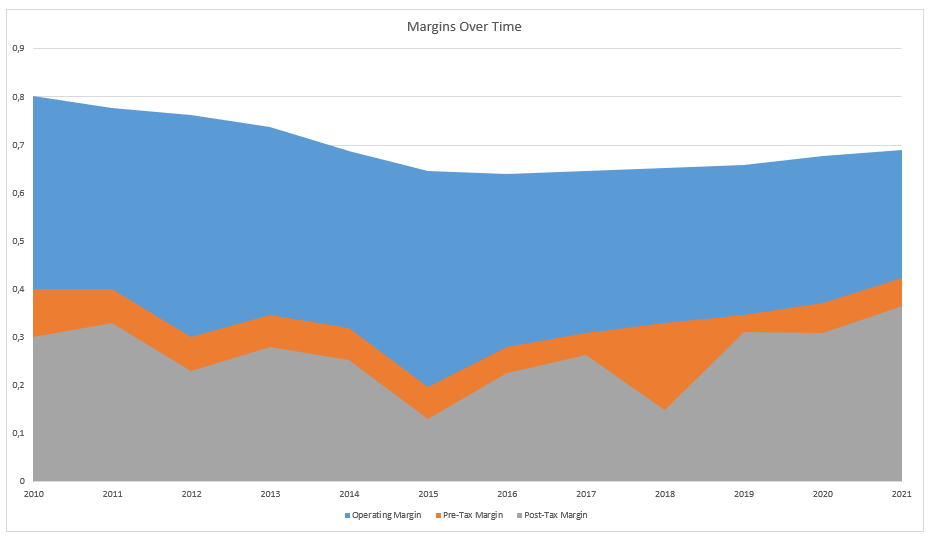

Margins

We’ve talked about this before in other deep dives, but I generally consider profit margins, and in particular pre-tax profit margins, to be the single best indicator of business quality when evaluating a company.

Ultimately a companies goal is to make money, and for that to happen, particularly in a consistent manner, the company needs to have reliable and consistent margins in their core business.

That’s not to mean that one part or another of the business can’t lose money, but if the business is not able to consistently maintain profit margins above 10%, then it is vulnerable not just to competition, but to any number of scenarios that might jeopardize its ability to operate.

Microsoft is not one of those companies.

Microsofts’ margins are one of the best in the world, and it is a perfect example of the desired scalability of technology companies.

Their operating margins, although slightly declining in the past few years, is head and shoulders above most other companies.

Their pre-tax Margin too is outstanding, being well above the 20% threshold that I use to judge if a company has an excellent business.

Growth

Earnings growth is alongside the payment of dividends one of the 2 factors responsible for substantially all shareholder returns over the past century.

In this area too Microsoft is a high quality business with a long track history of growth, and plenty of prospects for the future.

In here I would like to point out 2 things, first is the out-performance of earnings growth compared to both Revenue Growth and Pre-tax Earnings Growth.

While the out-performance is slight, and perfectly normal, it’s important to understand that every cent in Earnings comes from the Pre-Tax Earnings, which in turn is derived from Revenue.

An out-performance of Pre-tax Earnings compared to Revenue indicates higher margins, but those margins can get only so high.

The same applies to an out-performance of the Post-Tax earnings versus the Pre-Tax Earnings, companies may defer tax payments, and settle their affairs in such a way that minimizes their tax liabilities, but there is only so much they can do, and Uncle Sam wants his cut.

Per-Share Metrics

Finally we should have a look at the Per-Share metrics. This might not seem as important given the outstanding results we see in the previous 2 categories, however it is important to know that both the margins and the increased revenue and earnings are not hiding behind them something else.

Ultimately when we own a share in a company, we own a slice of that companies pie, but of course pies can be sliced in many different ways, and we need to make sure that not only is the pie getting bigger, but that our slice too isn’t getting smaller.

Fortunately both earnings per-share and outstanding shares are going up and down respectively. This is good for us, since it means our shares now own a larger piece of the pie, which is also getting bigger by the day!

Other Data

Now we can take a look at the some of Microsofts current data.

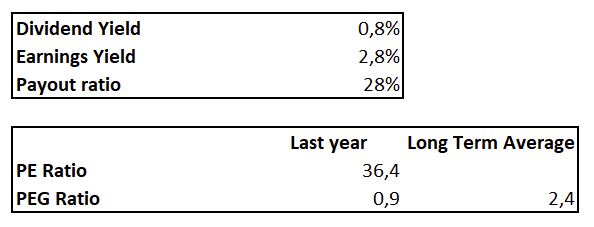

The first thing we should notice is that Microsoft is paying dividends, but their payout ratio is actually quite low under 30%.

Unfortunately at the current share price of $292 both the dividend yield and the earnings yield are low, and the PE (which is effectively a different way to formulate the earnings yield) is quite high at around 36.

While this is lower than last years pre-tax margin, its still a little bit higher than the 10 year average pre-tax margin. This means that using our standard Margin-to-PE method Microsoft could be seen as slightly overvalued.

But is that the case for every valuation metric?

Standard Valuations

Let’s take a look at the valuation that each of our standard methods gives for Microsoft.

The valuation Metrics that we will be looking at will be the following:

Historical Expected Return (Earnings Growth + Dividend Yield)

Margin to PE Method

Book Value

Ben Grahams (Revised and Original)

As you can see, the green highlighted numbers are the valuations that are above the current Microsoft share price, in red are the ones that are below.

For the most part it seems that the unusually high growth over the past year has enabled the valuation to go to higher levels than normal, but even still on a long term average Microsoft holds up well when it comes to both of Ben Grahams formulas.

This is because of a combination of historically low interest rates and unusually high growth.

This is in spite of a very high PE ratio, and an otherwise elevated long term average PEG ratio too.

Personally I would say that the Margin to PE method using last years earnings and the long term growth rate is probably the most accurate valuation, though one should apply an appropriate margin of safety before investing.

In addition to this, I also ran a custom “Discounted Earnings Model” that I will go into greater detail in the coming weeks. This model gives us the following results over the next 10 years:

The number you should focus there is in the second to last line, and is the “Discounted Total Return at Historical Market Average PE Ratio”, which is estimated at 1.2%.

In other words, this discounted earnings model expects Microsoft to severely under-perform the general market, and return a mere 1.2% annually over the next decade.

This is an unusual result, given the other valuations we’ve done, so it will require it’s own post. The general reason for this under performance is because the model assumes that Microsoft will have its PE ratio shrink back to the historical market average from its current outlier value.

Conclusion

Overall Microsoft is a high quality business whose valuation heavily depends on its growth, which has been unusually “super-charged” in the last year.

If Microsoft manages to keep growing at the current rate, then if will almost certainly be a fair investment with little chance to lose money, however given that it has been an outlier in terms of growth over the past decade, its current price and valuation is higher than the market average.

A return to the mean is fairly likely to happen over the next decade, just like we saw in the early 2000s. This means that it is possible for Microsoft to have its multiples shrunk to the market average (or below!), if this were to happen then even if the growth prospects are realized, it may well be that Microsoft will be a poor investment over the next 10 years.

Personally, I feel that that is the most likely option, and am therefore cautious in terms of investing in Microsoft at current prices, despite its bright and profitable business.

I feel that the margin to PE method is fairly accurate as to the companies fair value, and would therefore require a sufficient margin of safety from that in order to invest.

My current cost basis is a pricey $230. While I am not unhappy with my purchase, even that price is higher than I usually feel comfortable. I would definitely buy more if it went below $200 per share though, since at those values I would have a sufficient margin of safety.

What about you? How would you value Microsoft? How much would you say the company is worth?

Let me know what you think!

And as always, if you have any questions or comments, shoot them on Twitter @TiagoDias_VC or down below!

And of course, don’t forget to subscribe!