Intel Corporation - Part 3

The story of this company

Last week we valued Intel, an American Semi-Conductor designer and manufacturer that has dominated the market in the past decade, but which is now on a downtrend due to recent failures.

The Story

Intel is a big company with a lot going on, not only within itself, but within the industry it is doing business in.

Given the complexity involved with the company, I’m going to separate out their story into 5 different topics, and we’re going to talk about each of these individually.

These topics are:

R&D Failures

Intel Foundry and its core strategy

Chip shortages

Management and its quality

Geo-politics and state interests

This way we will be able to get a clear picture as to what is going on in the company, and what we can look forward to.

R&D Failures

Where to start here?

Ultimately Intels current problems begin and end with their repeated R&D problems since 2016.

I will not go deep into the history of their troubles, because it’s complex and I don’t think I would be able to do it justice. That said, if you're interested in the details, this medium post goes quite in depth about the matter.

Intel operated their CPU business on a Tick-Tock model for its most dominant years, with one “Tick” representing a new fabrication and process, reducing the die size, and the “Tock” the year after would provide needed optimizations that would take advantage of the size benefits in the new CPUs.

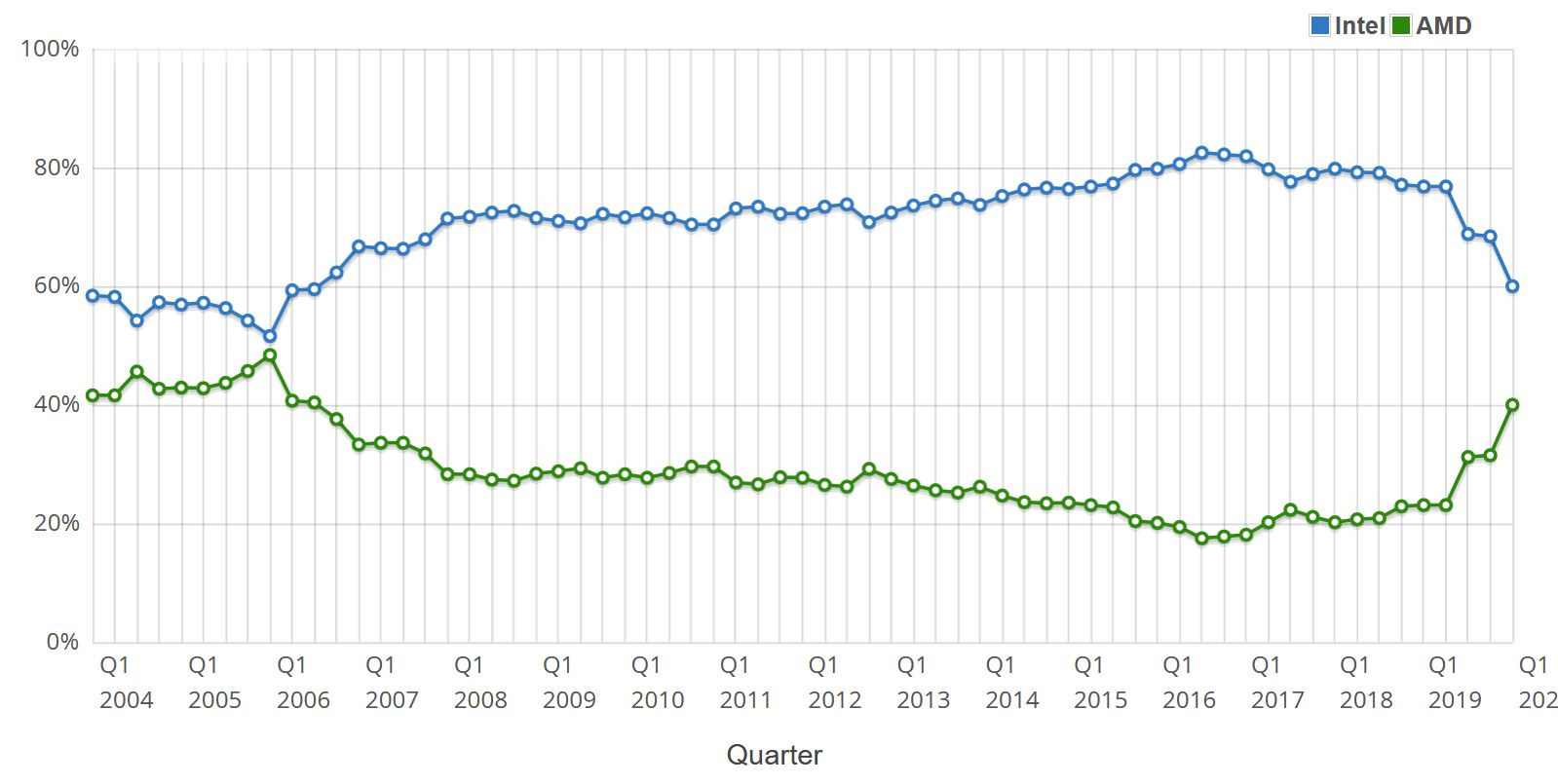

This allowed them to continuously decrease the size of their transistors, making their CPUs faster and better, and take their market share well into 80% of all CPUs sold by late 2016.

The problem was, the 10 nm Tick that was supposed to come in 2016 never did, and Intel has been stuck on 14 nm fabrication processes ever since.

They have been trying for years to get a working production ready follow up to their 14 nm fabrication processes for 5 years now, and at every point they have been unable to either design a new architecture, or their designs have been riddled with production issues resulting in very low yields which prevents their wide scale production.

And in the mean time, AMD has leapfrogged ahead of them, with a 7 nm fabrication process, and quickly increasing market share.

Intel has been doing an amazing job in maintaining and improving their existing 14 nm line up, so that it is still competitive with AMDs offerings, but particularly over the last year it has become increasingly clear that their 14 nm architecture is reaching its limits, and that smaller fabrication processes, or the lack of them, are a life or death issue for the company.

Ultimately whether Intel will continue to exist rests on its ability to finally bring in a new Tick, with a 7 nm fabrication process.

Which brings us to the main reason as to why their 10 nm and 7 nm processes have failed so far, their mass production in Intels foundries.

Intel Foundries and its core strategy

Unlike its competitor AMD, Intel also possesses a number of large scale foundries in which it produces the chips it designs.

This has its advantages, and their existence is key to the competitive advantages Intel had earlier in the decade. The control of process, from the design to its production was key in unlocking performance and streamlining the design, production and distribution of the chips, allowing higher margins and better products.

That being said, it also means that Intel is less focused than AMD, because whereas AMD is fully invested in designing the best possible chips, and can then shop around for the best option to produce those chips, Intel does not have that flexibility.

It also means that Intel is competing on two fronts, first with AMD on chip design, and second with TSMC (and Samsung and others) on chip manufacture.

This second market is also problematic because Intels R&D failures are intrinsically connected with their inability to manufacture their designs at scale.

Not only that, but keeping the in-house manufacture requires extremely heavy investments in new factories on the orders of tens of billions. They are and have been trying to reduce those costs by enabling a separate foundry business where Intel will manufacture chips designed by other companies, but that’s the same business model that TSMC is in, and one in which Intel has failed to gain ground over the last decade.

There have been calls for Intel to outsource its manufacturing needs to third party chip makers, similar to AMD, however while that would give some short term benefits, it’s important to realize that that would result in increased competition in the long term.

The in-house design and manufacture is a key portion of the long term Intel competitive advantage, and moving away from it, despite the cost savings, would be a big mistake.

Fortunately these R&D problems, and the in-house vs outsourced manufacture is a longer term concern, and in the short term, their current offerings are still competitive.

So now the question is, how long will they remain competitive? If we know that, we will be able to know how long Intel has to make a turn around.

Chip Shortages

Fortunately for Intel the 2020 pandemic has brought about a global chip shortage that could last until 2023 which is a major boon for Intel.

This major Chip shortage means that even if Intel chips are no longer the best on the market, they will still have as much business as they can fulfill for the next 3 years.

But we have to remember that Intel still has fairly reasonable performant chips on the market, and not only that but it has outstanding long term contracts with large clients.

These “good enough” chips and existing contracts will continue to provide it with free cash flow for the next few years, even if no further business arrives.

It’s difficult to estimate just how long Intel could carry on with no further orders, but given their backlog it’s not unreasonable to state that they could go for another year with no orders before they really start feeling the pressure.

And of course, a “no more orders” scenario is very unlikely in a normal year, let alone in a time of widespread shortages of the products Intel produces.

This combined with their existing contracts and cash flow should quite easily be able to tide them over for the next 5 years.

In other words, if during the next 5 years Intel comes out with microprocessors that are competitive with AMD, they will be just fine.

Admittedly this isn’t a consensual statement. The continuous delays in R&D, and issues productionizing the chips has already caused some clients to be lost, some of them permanently. Additionally it has made competitors more attractive and that too has been causing troubles, which will continue in the far future.

Apples move away from Intel chips has been a watershed moment here, and Microsoft investments in the space, Qualcomms entries in the 5G modem are very concerning.

Ultimately only time will tell if Intel is living on borrowed time, or if they will be able to make use of this time and chip shortage to jumpstart their business back up.

Whether they succeed or fail will be determined by the quality of their management…

Management and its Quality

Bob Swan has been removed as CEO of Intel and replaced with Pat Gelsinger.

Swan wasn’t a terrible CEO in my eyes, although I’m sure there are many who would disagree. He was handed a poor situation by the untimely departure of his predecessor Brian Krzanich, who was forced to resign in 2018 due to unprofessional conduct with other Intel employees.

That being said, both Brian Krzanich and Bob Swan had their heads in the right place, and kept shareholder value as a high priority. They drove Intel through a period of increasing dividends, and share buybacks which created a lot of value.

The issues in R&D are often attributed to poorly considered cost cutting, however R&D is difficult, and Intel has consistently ramped up their spending there year over year over the past decade.

Personally I think it was just a combination of bad luck, and some poor decisions on where to take the next few generations of chips that caused their delay. The financial performance of the company wasn’t the issue, the issue was R&D, and the board clearly recognized that, and it clearly recognized that shareholders were not satisfied with Swans performance in that respect..

That being said, it is clear that the market approved of the ousting of Bob Swan, Intel shares rose almost 8% immediately following the news.

I don’t think he was a bad CEO, but i also don’t think he was the CEO Intel needs right now.

So, who is his replacement? Who is Pat Gelsinger?

Gelsinger is an old hand at Intel, having been a part of it for over three decades before jumping ship to head up Dell and then VMWare.

During his 30 year tenure at Intel he became its first ever Chief Technology Officer, and helped establish Intel’s Market leadership.

His role at VMWare was characterized by incredible revenue growth, and his experience is indisputable. His technical background too means he is more likely to make good decision when it comes to fixing the R&D, and he has already done moves that show he has a clear strategy for the company.

Out of all CEOs Intel could possibly get, I think Pat is probably the best for the company at this time. If anyone can turn this ship around, he will.

Geopolitics and State Interests

Finally, we need to talk about the elephant in the room.

Microprocessors are everywhere, and so its natural that countries and governments take particular interest in not only securing their own supply, but also in ensuring that their geopolitical adversaries do not.

The American-Chinese rivalry is key to understand what is happening here.

China in particular has been focusing on producing chips internally for the past few years, and it’s seen as a top governmental priority. The American sanctions on Huawei serving to underscore the need for self-sufficiency in terms of electronics manufacture.

In the same way Taiwan sees TSMC as key to its security from invasion across the strait. By making the world depend on TSMC for chips, they can ensure that a mainland invasion will result in an International response. This national interest is part of the reason as to why during a drought, TSMC has been allowed to truck in water in order to continue producing their chips.

All the same, the US wants to reduce this dependence, which is why TSMC has also begun work on building factories in the US. This US push for on-shore manufacturing of semiconductors is rightfully seen as of national interest, and so it presents an opportunity for Intel.

In fact, the US has passed bills encouraging and funding this, and Intel, with its in-house manufacturing and design is perfectly poised to take advantage of these grants.

While the restrictions involved might make it less attractive to its competitors, the close and long standing relationship between Intel and the US government, alongside its in-house strategy means that Intel will not be as harmed by them as its competitors, and so it will be able to make better use of the US governments need for onshore design and manufacture.

And that is just in time to assist Intel with the multi-billion dollar effort to renew and revamp its foundry business.

The Verdict

Should we buy Intel?

I bought Intel, so the verdict is an obvious Yes.

It’s clear to me that Intel is an undervalued company that can make a turnaround from its problems if only one of its catalysts are successful. As far as I can see, if they get just one win over the next 5 years, they will be able to compete with AMD, and maintain their high profitability.

Their dividend is well covered by their earnings, and while they might need to ramp down their share buybacks in order to invest in their new US factories, I fully expect that investment to pay dividends in the future.

Do you agree? Do you Disagree?

Are you buying, selling or holding?

Let me know what you think!

And as always, if you have any questions or comments, shoot them on Twitter @TiagoDias_VC or down below!

And of course, don’t forget to subscribe!

Great analysis! Long Intel - I agree with your thesis!

Great piece of work! I have myself a position in Intel, AMD and Micron, so I hope all do well.