Debt and You

Do you have a plan?

It’s no secret that I don’t like debt, both in the companies that I own, and in my personal life.

I don’t have any credit cards, I don’t have any mortgage, I don’t owe friends or family money.

The closest thing I have to a debt is a pair of bets with some friends on which companies will outperform over the next 5 years. The total amount at risk there is a couple of beers.

Debt is a bad thing, and you should avoid it wherever you can.

I want to be clear here:

If you’re in your late 20s and you have any amount of consumer debt you need to have a serious look in the mirror and figure out where you went wrong, and what you need to do to change it.

Debt is not something you want to have hanging over you if you can help it, and so when you have debt that isn’t productive, all that you’re doing is hamstringing your future self.

That’s not to mean that debt is intrinsically bad, certainly you can have productive debt.

Perhaps you borrowed money to invest in something that will provide you a return that you can use to pay back the debt.

That return can come in many ways, including by replacing some expenses that you were otherwise guaranteed to have, such as a mortgage being used to buy a house that would replace (part of) your housing expenses.

Of course the issue here is that it has to actually replace actuals expenses that you would actually and unavoidably have.

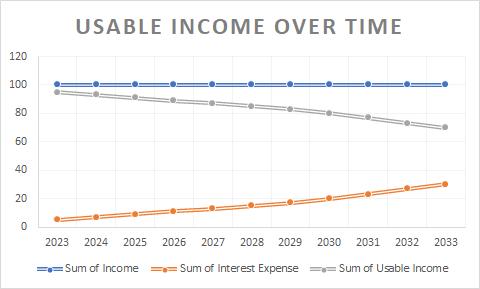

Overall though you need to understand debt as no more than renting capital, and that rent is a fixed expense that will take part of your income from you every single month until it is paid off.

If you don’t pay off that debt, and particularly if you keep accumulating debt…

Your usable income will decrease more and more.

That’s money you can no longer use to save, enjoy, or pay off debt, resulting in a debt spiral that will progressively worsen your financial quality of life.

So what you need to do in order to have more income… Is to pay off that debt.