Automatic Data Processing

A fully integrated bet on the labor market

Key Data

Ticker Symbol: ADP 0.00%↑

Price: $229

Market Cap: $94 Billion

Forward Dividend: $5.00

Dividend Yield: 2.2%

Payout Ratio: 59%

Areas of operation: Worldwide

Sector: Industrials - Staffing & Employment Services

Business

Automatic Data Processing, ADP 0.00%↑ , is an American provider of Human Resources Management software and services. With almost a million clients in over 140 countries, this company does everything from payroll, compliance and software related to Human Capital Management.

ADP is actually the payroll provider that the company I work for uses, and so I see their logo every month when I receive my payslip!

ADP is in many ways a combination of a software company with a financial services company.

Their business has 3 key parts:

Human Capital Management Solutions (HCM)

Human Resources Outsourcing Solutions (HRO)

Global Solutions

Each of these distinct groups has different, but interrelated focuses.

HCM is your standard suite of Human Resources software that is licensed and provided as a service to businesses of all sizes. In this sector the HR tasks and responsibilities fall solely on the client's side, and ADP software is used to keep track of and allow the client to self-manage their own HR department.

HRO is a far deeper integration of ADP into the clients business, and is most well exemplified by their “Professional Employer Organization” (PEO) offer. As per their 10-K:

With a PEO, both ADP and the client have a co-employment relationship with the client’s employees. We assume certain employer responsibilities such as payroll processing and tax filings, and the client maintains control of its business and all management responsibilities. ADP TotalSource clients are able to offer their employees services and benefits on par with those of much larger enterprises, without the need to staff a full HR department.

In short it’s a full outsourcing of your HR department onto $ADP, rather than merely using software provided by ADP .

Finally the Global Solutions consists of multi-country and local in-country solutions for employers. In short, if you want to hire people outside of your native country, you can make use of ADP global solutions to handle the regulatory, tax and other compliance concerns that result from that.

Each of these sectors has distinct business economics, with its own quirks.

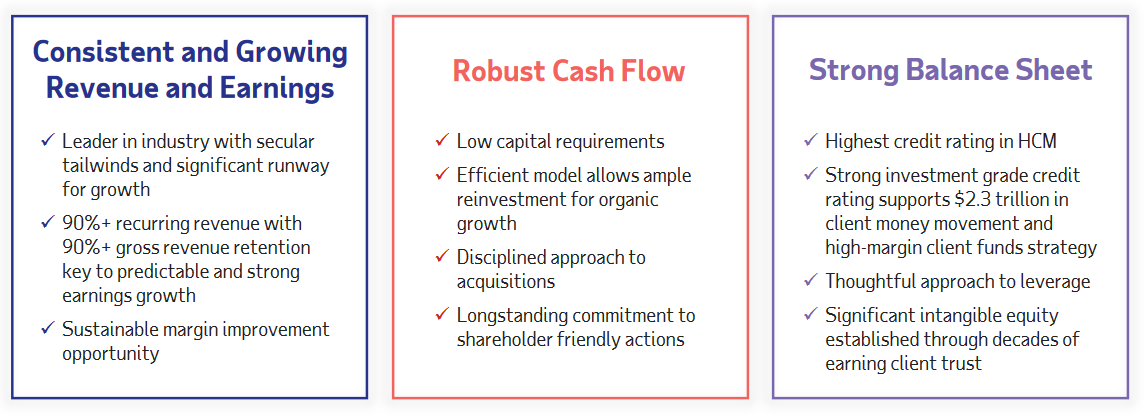

HCM is the simplest to explain because it essentially functions as a subscription based business model where companies pay per month a fee which consists of a fixed amount plus a per employee amount.

There’s different options and different types of software, but ultimately this is a subscription model that grows as the client grows, and which provides stable and reliable cash flow on a monthly basis.

HRO is slightly different, since in many cases there is a co-employment of employees, something that goes well beyond software.

In many cases ADP collects money from clients, holds it for some time receiving interest on it, and then distributes it to employees and governments as wages and taxes. This is a similar idea to the float that insurance companies use.

This is a very sticky subscription model, with additional fees and interest coming in on the side. It’s essentially impossible for clients to move away from ADP, since it would require them to rebuild their entire HR from scratch.

The large amount of cash held for clients too means that the companies assets and liabilities are inflated well beyond their otherwise capital light business would suggest.

Finally their global solutions function primarily on the basis of fees, and again subscription income.

The underlying economics of this business is solid, and should generally track the economics of the overall employment market. Additional labor regulations are actually quite good for the business, since it enables them to up-sell additional compliance services.

Management

Maria Black is the President and CEO of ADP, having been appointed to the role in 2023. She has been with the company since 1996, having joined as a sales associate. She has been with the company for decades and has deep knowledge of the business.

From an insider sales perspective the company has seen substantial movement over the past few years, with many insiders including Maria having sold substantial portions of their ownership in the business (as well as options they received as part of their compensation package).

This isn’t great since it might indicate that the company may be overvalued, but at the same time it isn’t necessarily a deal breaker.

Key Risks and Opportunities

Risks:

Changes to laws are common and may impact the business model

Heavily dependent on outside factors such as the labor market health for their revenues

The company makes heavy use of data, and subsequently exposed to security breaches.

Opportunities:

Asset light

Extremely sticky subscription business model

Stringent regulation is a key moat

Financial Data:

Shareholder Returns:

Dividends

The company pays a $5.00 dividend.

The company has increased it dividend yearly for 24 years.

The company has increased it’s dividend over the past 5 years at a 13% CAGR.

Share Buybacks

The company conducts regular share buybacks

The company has bought back 1.9 Billion in shares in 2021

Shares outstanding have reduced by 1.6% in 2021

Income Statement:

Revenue Growth Rate

Long Term - 8.3%

3 Year - 10%

Revenues are reasonably solid and stable, while growing at impressive rates.

Pre-Tax Profit Margins

Long Term - 17%

Return on Assets

Last Year - 6%

This figure is deceptive due to the huge amount of operational leverage used.

EPS Growth Rate

Long Term - 14%

3 Year - 23%

Cyclicality

Non-Cyclical

Cash Flow Statement:

Operational Cash Flow Growth Rate

Long Term - 9%

3 Year - 2%

Stock based compensation has been growing, and comprises 6.5% of operating cash flows (201 million vs 3099 Million)

Investing Cash Flows Growth Rate

Investing Cash Flows are highly cyclical due to changes in client funds obligations resulting in purchases of marketable securities

There are no major capex

Financing Cash Flows Growth Rate

Changes in client funds obligations heavily impact financing cash flows, and are unrelated to $ADP itself

Balance Sheet:

Assets:

Main Assets are funds held for clients.

The majority of assets are cash and equivalent current assets with high liquidity

Liabilities:

The main liabilities are the client funds mentioned above.

There is a slight mismatch between those assets and obligations, implying some directional risk

Debt:

No substantial long term debt

No Debt Cliffs

Valuation:

Key Metrics:

Bullish

Discounted Earnings - $925

Discounted Cash Flow - $1762

Margin to PE - $161

Market Multiple - $226

Cash Multiple - $634

NCAV - $7

Bearish

Discounted Earnings - $98

Discounted Cash Flow - $187

Margin to PE - $96

Market Multiple - $57

Cash Multiple - $45

NCAV - ($45)

Average

Discounted Earnings - $262

Discounted Cash Flow - $500

Margin to PE - $108

Market Multiple - $93

Cash Multiple - $295

NCAV - ($12)

For the average assumptions when it comes to the Discounted Earnings and Discounted Cash flow numbers I assume a revenue growth rate of 8%, net margins of 21%, cash margins of 40% and a discount rate of 11%.

The bullish/bearish stances generally impact those assumptions by 30% each way. The same applies to the other valuation methods.

Expected Value:

The valuation that’s closest to reality is probably the Average Discounted Earnings valuation, since we’re buying this company for the earnings it generates, and there are no meaningful barriers to its continued growth, and the company appears to have a solid built-in moat to its business model.

That said, when we aggregate all Average valuations into a single average value we expect a fair value of $208.

Assuming a 30% margin of safety, I would expect that the company would be a somewhat secure investment at $144 per share.

This would provide a 3.4% dividend yield.

Investment Thesis

The company provides software and services that are highly sticky and key to their clients businesses

The profit margins are relatively high indicating some degree of pricing power

Regulatory requirements, and the deep integration between ADP 0.00%↑ and the clients business provide an almost insurmountable moat to compete against

Much of the business is composed of “pass throughs” for which the company collects a fee and interest

The management team is qualified

The company is likely overvalued at this time

Decision

Current Stance: HOLD

I don’t currently own ADP 0.00%↑ , but if I did I would be a happy owner. Ultimately the company is in no danger of bankruptcy, and it has demonstrated a commitment to returning capital to shareholders.

While there may be better options out there, the growth in the business, alongside the deep moat means that selling out of the company wouldn’t be a good idea. At the same time the high valuation makes it hard to justify any additional investment.

Do you have a different view on the company? Are you buying, selling or holding?

Let me know down below!

What is your view on competition such as $WDAY?