Altria - Part 2

Valuing the last few puffs of this cigarette butt

Last week we talked a bit about Altria, an American cigarette manufacturer with high margins that is currently out of favor with investors.

Today we’re going to be going over some of their numbers and calculating how much this company might be worth.

The Usual Valuations

We’ve done this before, so I won’t go into details on how these numbers were calculated. If you’re interested in learning more about how it was calculated, I suggest taking a look at some of my previous deep dives.

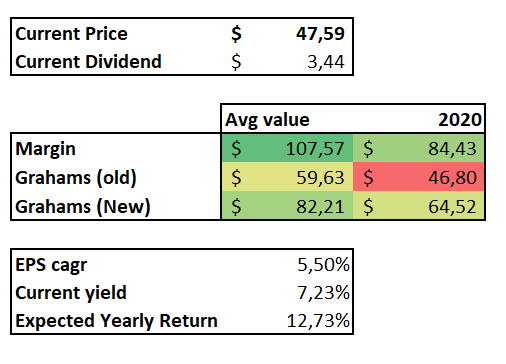

The first thing that should jump out at you is the red values when it comes to the 2020 valuation using Ben Grahams old formula. What that indicates is that Bens formula is valuing the company at $46.80 per share, compared to the current price of $47.59.

The reason for this “low” valuation for this specific model, is because of the unusually low 2020 earnings.

To be perfectly honest I do not consider that an accurate valuation of the company, nor do I consider any of the 2020 numbers to be reliable for a simple reason:

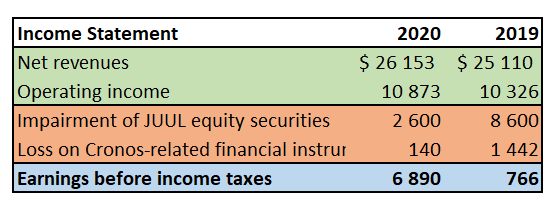

Altria had major impairments in the past 2 years, which will likely not be repeated.

In other words, their earnings last year would have been almost 40% greater had it not been for this non-cash charge. For 2019 the situation was even worse and their earnings would have been over twelve times what they otherwise would have been.

These impairments were the result of regulatory changes, and we will discuss them next week when we talk about the companies story. Today I will only say that I don’t believe these impairments reflect negatively on either the financial performance of the company, or on the quality of its management.

Another thing you might have noticed was that little entry at the bottom of the first table:

If you’ve been reading the blog for some time now, you may recognize the way that I calculated the “Expected Yearly Return”, it’s actually a very simple calculation.

All I did was take the 10 year average Compound Annual Growth Rate of the Earnings per Share (5.5%) and added the current Dividend Yield (7.23%) to that number.

In other words, the expected return of this company is a function of the dividends that the company pays out, and the increased ability to pay those dividends. See this blog post for additional information on that.

This isn’t extremely accurate, after all dividends can be cut, and past earnings growth may not be followed through into the future, but it’s still a decent ballpark figure that is mostly accurate as long as the company continues to progress the way it has over the past 10 years.

The Balance Sheet

We’ve seen this before, but it’s worth taking another look at the balance sheet of Altria:

Altria is running a tight and lean business, and returns substantially all of its earnings to shareholders via either dividends or share buybacks.

You can see the effect of the buybacks in the “Cost of Repurchased Stock” section, where just about every dollar that was “reinvested in the business” was used to buy out our partners (and thereby increasing our ownership of the company).

I’m not the biggest fan of stock buybacks, due to the way that they can be used to unfairly benefit management, however given Altrias longstanding history and commitment to share buybacks, I’m not too concerned about the possibility that they are strategically conducting buybacks for their own personal benefit rather than the common shareholders.

Unfortunately what this lean approach also means is that the company isn’t keeping its earnings, and therefore its book value is not meaningfully increasing.

This means that Altria, unlike say Aflac, does not have substantial amount of capital just “lying around” and a Net Current Asset valuation will not be particularly attractive.

The Margin of Safety

The margin of safety is a concept we’ve discuss briefly before, but one that should not be ignored in any discussion regarding investing in a specific issue.

Ultimately as investors our returns will necessarily be the difference between the true value of a business, and how much money we paid to own that business.

It’s important to recognize that how much you pay for a business is just as, if not more important than the underlying quality of the business itself.

A business, even a failing one may still be a 100x’er or 200x’er if it is being sold at 1/100th or 1/200th of its real value.

After all, even a business which is not expected to generate any further revenue, may sell its assets and distribute the resulting gains to its owners before being dissolved.

We’ve talked about this “Net Current Asset Value” when we discussed Aflac before, and the “Net-Net” investment strategy does tend to have good results, even with under-performing (or bankrupt!) businesses.

In the same way, even the best and most profitable business in the world may be a terrible investment if you pay more for it than you will ever get back.

Knowing that, we must be aware of what our margin of safety is in order to determine if a business is being sold at an attractive price or not.

This “current margin of safety” can be calculated by simply seeing the difference between the expected value of the company, and how much it is being sold for.

As you can see, if we disregard 2020, and count only the 10 year average, we have quite an attractive margin of safety, that is over 20% even in the worst model.

If we account only for the 2020 numbers, with the exception of Grahams old formula where we are paying roughly what the company is worth, we still have quite an attractive margin of safety when using either the Pre-tax profit margin method, or Grahams new method.

Conclusion

Given that the net tangible assets of the company, as per the balance sheet, are effectively zero, we will mostly be looking at Altria as a source of cashflow, that is, we will be buying it for its earnings, and the cash that is provided to us in the form of dividends and share buybacks.

So what is the actual value of this company?

Like most valuations, its a bit uncertain. Personally I prefer the pre-tax profit margin method, but I can understand why others may choose to use a more traditional discounted cash flow model, or some other method.

That said, I’m inclined to believe the true value of the company is somewhere between the results given by the 10 year average margin model ($107) and Grahams old model ($59).

Whatever the case may be, it looks like we have sufficient margin of safety, and an investment there may make financial sense.

Whether we should invest in it will ultimately depend on the final section of this deep dive, the one focusing on the companies story, which we will get to next week.

What about you? Do you smoke? Are you an Altria client?

Let me know what you think about the company and their products!

I’ve also been participating in the European Investor Network, so if you’re in the mood for more content from me and other European investors, have a look because you won’t be disappointed!

And as always, if you have any questions or comments, shoot them on Twitter @TiagoDias_VC or down below!

I’ll see you next time!