A look back at Intel

Reviewing my semiconductor turnaround play

About a year ago I had a first look at Intel, and decided to buy the company after doing my valuations and seeing that it looked undervalued.

It’s now been a year, the stock price is down 20%, and many investors would be panicking right about now, so it’s time to take a look back at my thesis, see how its played out, and the next steps to take should be.

The thesis

Let’s take a look back at what I wrote a year ago to see what I thought about the company, and what the thesis for it would be:

The company has solid financials and is unlikely to go bust soon

The company has fallen behind in R&D but is trying to catch-up

The companies foundry strategy is key to their competitive advantage and should not be abandoned

The chip shortages will benefit Intel, and give it enough runway to catch up in R&D

The company will continue its shareholder friendly dividend policy

Intel will benefit from state subsidies

How has this held up?

Let’s take it point by point:

The company has solid financials and is unlikely to go bust soon

Well, the company hasn’t gone bust yet!

In fact if we take a look at the latest quarterly report, and compare it with the 2020 annual report I used at the time to check the viability of the company, we can see that the companies shareholders equity has increase substantially, whereas their debt has actually decreased!

Their net revenue has slightly increased in 2021 over 2020, though higher operating expenses and restructuring charges caused net income to be slightly under 2020.

Still, the company is currently in no danger of bankruptcy or financial trouble.

The company has fallen behind in R&D but is trying to catch-up

This is still true, however there are some encouraging signs that their R&D is finally coming back, and from what I can tell their consumer CPUs are now on par with the best AMD CPUS.

There’s still a long way to go, especially when it comes to smaller transistors, but they are on the right track.

The companies foundry strategy is key to their competitive advantage and should not be abandoned

It’s clear that Intel is not abandoning their foundry strategy, and they have continuously come out with new initiatives to publicize and gain market share in that segment.

The chip shortages will benefit Intel, and give it enough runway to catch up in R&D

And they have! Shortages remain, and revenues have continued to go up throughout.

We still have at least another year of these shortages left, and Intel will continue to benefit from them!

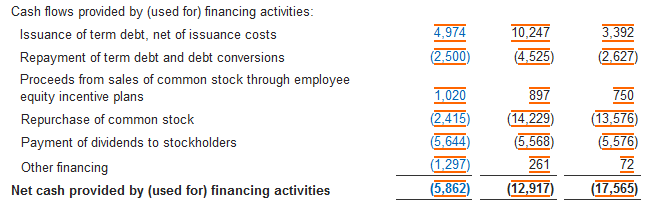

The company will continue its shareholder friendly dividend policy

And they have!

The company continued to pay their dividend, and even raised it in 2021!

Their share buybacks however were severely reduced, and the cash was re-routed for additional CAPEX and other investing activities.

This is sad, but ultimately the right move. We knew going in they would need to spend heavily on R&D and other CAPEX.

Intel will benefit from state subsidies

Well, they are.

They are getting tons of subsidies not just from the US, but from EU countries, etc…

As per Pat Gelsinger himself:

“Our planned investments are a major step both for Intel and for Europe. The EU Chips Act will empower private companies and governments to work together to drastically advance Europe’s position in the semiconductor sector," said Intel CEO Pat Gelsinger. "This broad initiative will boost Europe’s R&D innovation and bring leading-edge manufacturing to the region for the benefit of our customers and partners around the world. We are committed to playing an essential role in shaping Europe’s digital future for decades to come.”

The future

Overall my thesis remains the same, and it has continued to play out about what I expected.

It’s core value proposition is:

The company is reliably profitable

It will return capital to shareholders

It was severely undervalued considering the quality of its business and its growth

All of these things have continued to be the case 1 year later, regardless of the 20% drop in share price, so if the fundamentals of the business haven’t changed, and my thesis still holds, why would I change my stance?

I’ll continue to hold the business, and once I have finished dealing with the portfolio allocation issues I’ve discussed previously, I will likely purchase some additional shares.

That bit crossed out above was my stance up until this week, when Intel kept going down, and began trading at $40.54. This is wildly undervalued, and I’ve since purchased 50 additional shares.

My Stance: BUY

What about you? Do you like Intel? Do you think they are turning the ship around?

Let me know in the comments below!